The Corporate Transparency Act (CTA), enacted by the US Congress, came into force in January 2021. On January 1, 2024, the CTA introduced corporate ownership reporting requirements in the US for the first time. This mandates that corporations, limited liability companies, and similar business entities file information about their beneficial ownership with the Financial Crimes Enforcement Network (FinCEN).

Beneficial ownership information (BOI) is a key element in enhancing corporate transparency and preventing the misuse of companies for illegal activities. These BOI reporting requirements apply to both foreign and domestic companies registered to do business in the United States. Each reporting company must submit information about the company and its beneficial owners. This guide delves into the various aspects of BOI, explaining what it is, why it is important, who has access to it, how to report it, and more.

Why was BOI Reporting Introduced?

The introduction of BOI (Beneficial Ownership Information) Reporting is a critical component of enhancing U.S. national security and safeguarding the financial system. This initiative, part of the Anti-Money Laundering Act of 2020 and the Corporate Transparency Act (CTA), mandates that companies disclose their beneficial owners to FinCEN. By increasing transparency, this measure helps law enforcement and national security agencies identify and investigate illicit activities such as narcotrafficking, human trafficking, fraud, and identity theft.

FinCEN utilizes advanced analytic tools to examine these reports, map illicit networks, and issue public alerts to enhance reporting from the financial sector. Non-compliance or false reporting can trigger investigations, while accurate disclosures prevent the exploitation of corporate anonymity, ensuring a more secure and equitable financial environment.

Understanding Beneficial Ownership Information

Beneficial ownership information helps to identify details of individuals who directly or indirectly own or control a company, including personal information such as names, addresses, dates of birth, and identifying numbers of the beneficial owners. The primary goal of collecting BOI is to promote transparency and combat financial crimes like money laundering and tax evasion by tracing the true owners of corporate entities.

Importance of Reporting Beneficial Ownership Information

The US Congress enacted the CTA in 2021, which introduced a mandatory BOI reporting requirement. This legislation is part of the government’s broader efforts to deter illicit activities that exploit the anonymity provided by shell companies and complex ownership structures. It makes it harder for bad actors to hide behind these entities; the act aims to safeguard the financial system from abuse.

Access to Beneficial Ownership Information

Access to BOI is strictly controlled to ensure confidentiality and security. The following entities are authorized to access BOI:

- Federal, state, local, and Tribal officials

- Certain foreign officials, through a US Federal government agency

- Financial institutions, with the reporting company’s consent

- Regulators supervising financial institutions

FinCEN stores BOI in a secure, non-public database protected by rigorous security measures typical of high-level federal information systems. It ensures that BOI is used only for authorized purposes and remains confidential.

Company to Report its Beneficial Owners

All companies are not required to report BOI to FinCEN under the reporting rule. A reporting company is any entity that does not qualify for an exemption and meets the “reporting company” definition. There are two types of reporting companies: “domestic reporting companies” and “foreign reporting companies.” If your company does not meet the criteria for either category or qualifies for an exemption, it is not required to file a BOI report with FinCEN.

Reporting Company

Reporting companies includes both domestic and foreign entities and are required to report beneficial ownership information to FinCEN.

Domestic reporting companies includes limited liability companies (LLCs), corporations, and any other entities created by filing a document with a secretary of state or similar office within the United States.

Foreign reporting companies are entities, such as corporations and LLCs, formed under foreign laws but are registered to do business in the United States by filing a document with a secretary of state or similar office.

Special Cases: Trusts, Business Trusts, and Foundations

Whether a statutory trust, business trust, or foundation is considered a reporting company depends on its creation process. A domestic entity like a statutory trust or foundation is a reporting company only if it was created by filing a document with a secretary of state or similar office. Similarly, a foreign entity is a reporting company only if it is registered to do business in the United States by filing such a document. State laws vary on whether certain entities require filing with the secretary of state for creation or registration. For example, if a trust is established in a jurisdiction requiring such filing, it is considered a reporting company unless it qualifies for an exemption. Companies should also consider potential exemptions to the reporting requirements, such as the tax-exempt entity exemption.

Trust Registration with Courts

A trust that registers with a court of law solely to establish jurisdiction over disputes does not become a reporting company. Registration for this purpose does not meet the criteria for creating a reporting company under FinCEN regulations.

Impact of Company Activity or Revenue

The activity or revenue of a company can sometimes determine its status as a reporting company. A reporting company is defined as any LLC, corporation, or similar entity created in the United States by filing a document with a secretary of state or similar office or any foreign entity registered to do business in the US by such filing, provided it does not qualify for any exemptions. An entity’s activities and revenue can qualify it for an exemption.

For instance, entities with gross receipts or sales in the previous year exceeding $5 million or those engaged in passive activities like holding rental properties may qualify for specific exemptions.

Sole Proprietorships

A sole proprietorship is not considered a reporting company unless it was created or registered to do business in the United States by filing a document with a secretary of state or a similar office. It’s important to note that obtaining an IRS employer identification number, a fictitious business name, or a professional license does not create a new entity. Consequently, these actions do not make a sole proprietorship a reporting company.

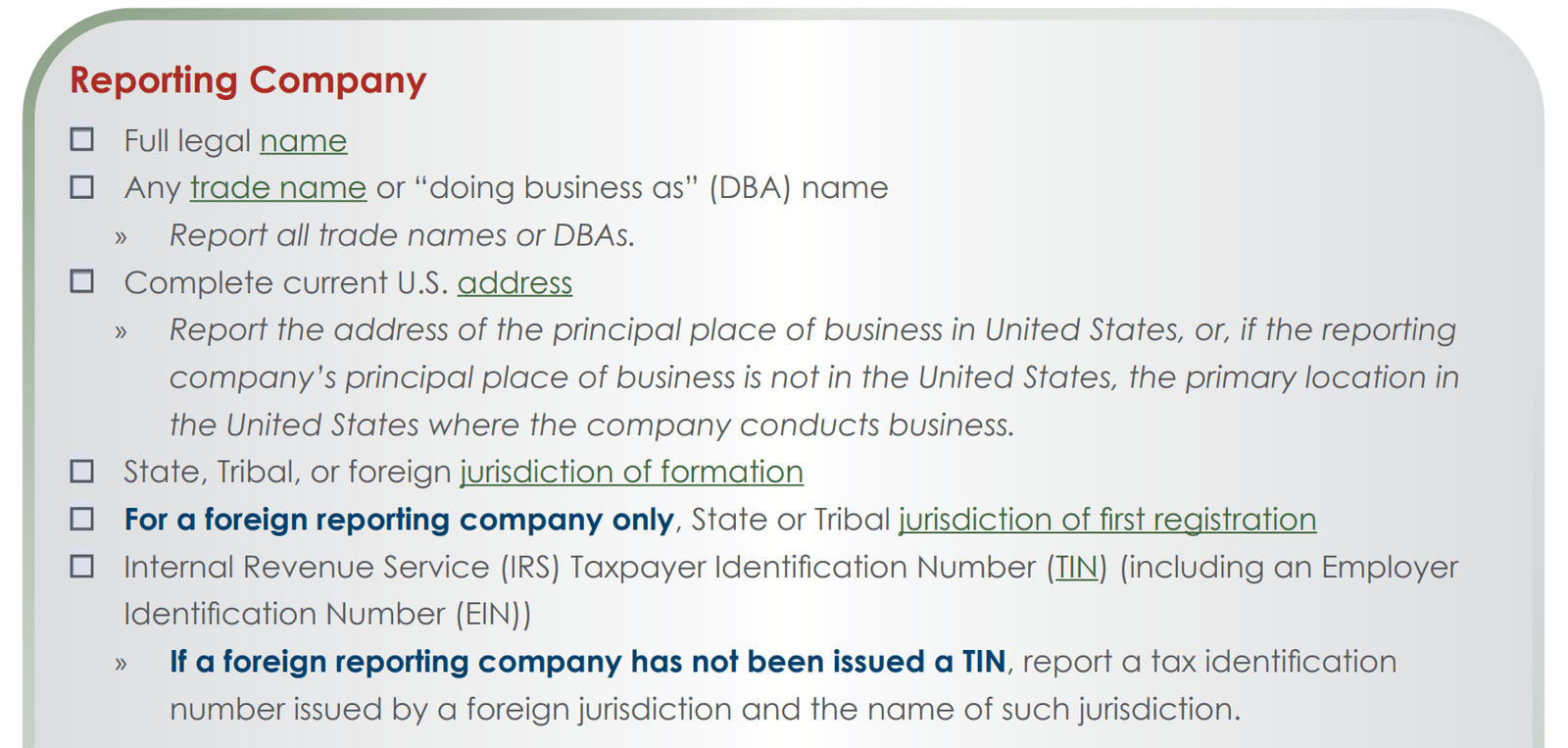

Information Required About the Reporting Company

When filing a report, a company must provide several key pieces of information:

- Legal Name: The official name under which the company operates.

- Trade Names: Any alternative names or “doing business as” (DBA) names.

- Principal Place of Business: The street address of the company’s primary location. For U.S.-based companies, this is the address of their headquarters, while foreign companies must provide the address of their US business location.

- Jurisdiction of Formation: The state or country where the company was legally formed or registered.

- Tax Identification Number: This includes a Taxpayer Identification number (TIN), US Employer Identification Number (EIN) or, for foreign companies, a tax identification number from their home jurisdiction.

Additionally, the report should specify whether it is an initial filing, correction, or update of a previous report.

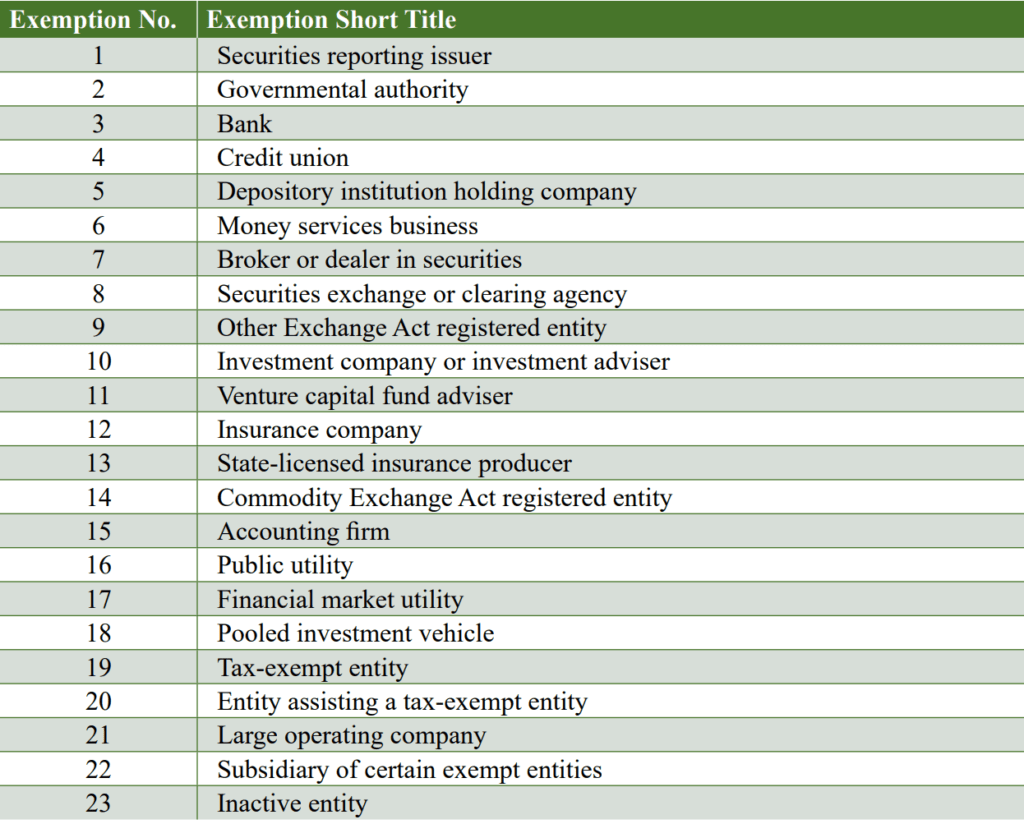

Reporting Company Exemptions: Criteria and Procedures

Certain entities are exempt from the reporting requirements for beneficial ownership information. There are 23 specific types of exempt entities, including securities reporting issuers, governmental authorities, banks, credit unions, and large operating companies, among others. For example, entities such as insurance companies, public utilities, financial market utilities, and tax-exempt organizations fall under these exemptions.

Each exemption has specific qualifying criteria that must be reviewed thoroughly before a company can conclude it is exempt.

Certain entities are exempt from the beneficial ownership information (BOI) reporting requirement based on their tax status. To qualify for the tax-exempt entity exemption, an entity must meet one of the following criteria:

- 501

(C)Organizations: Entities described in section 501(C)of the Internal Revenue Code (Code) and exempt under section 501(a) of the Code. - Recently Lost Tax-Exempt Status: Entities described in section 501

(C)that were exempt under section 501(a) but lost this status within the last 180 days. - Political Organizations: Entities defined as political organizations under section 527(e)(1) of the Code, and exempt under section 527(a).

- Certain Trusts: Entities that are trusts described in paragraphs (1) or (2) of section 4947(a) of the Code.

Inactive Entity Exemption

An entity qualifies for the inactive entity exemption if it meets all of the following criteria:

- Existence Before January 1, 2020: The entity existed before this date.

- Not Engaged in Active Business: The entity is not involved in active business operations.

- No Foreign Ownership: The entity is not owned by a foreign person.

- Stable Ownership: No changes in ownership in the past 12 months.

- No Significant Transactions: The entity has not sent or received more than $1,000 in funds during the past 12 months.

- No Assets: The entity does not hold any assets or ownership interests in other entities.

Subsidiary Exemption

A subsidiary may be exempt from BOI reporting if it is wholly owned or controlled directly or indirectly by one or more exempt entities, including:

- Securities reporting issuers

- Governmental authorities

- Banks and credit unions

- Investment companies and advisers

- Insurance companies

- Public utilities

Large Operating Company Exemption

The large operating company exemption requires that the entity:

- Employs more than 20 full-time employees in the US.

- Has filed a Federal income tax return in the previous year showing more than $5,000,000 in gross receipts or sales.

- Maintains an operating presence at a physical office in the US.

Entities cannot consolidate employees across multiple companies to meet this criterion.

Reporting Exempt Status

If a company qualifies for an exemption after having previously filed a BOI report, it should file an updated BOI report to indicate its newly exempt status. This updated report only requires the entity to identify itself and check a box noting the exemption.

Partial Control by Exempt Entities

A subsidiary must be entirely owned or controlled by exempt entities to qualify for the subsidiary exemption. Partial control by an exempt entity does not qualify the subsidiary for this exemption.

Fluctuating Company Size and Reporting Requirements

A company that fluctuates above and below the large operating company thresholds must file a BOI report when it does not meet the exemption criteria. If the company qualifies for an exemption at any point, it should file an updated BOI report indicating this status. If the exemption criteria are no longer met, the company must file an initial BOI report within 30 days of the change.

Public Utility Exemption

Entities classified as regulated public utilities, including those providing telecommunications services, are exempt from BOI reporting. This includes corporations providing telephone or telegraph services if they meet specific regulatory requirements.

Filing Federal Tax Returns and Exemptions

If a company has not yet filed its Federal income tax return for the previous year, it should use the return filed in the previous year for determining exemption eligibility. Should a tax return demonstrate less than $5 million in gross receipts or sales, the company must file a BOI report within 30 days.

Who is a Beneficial Owner?

A beneficial owner is an individual who either directly or indirectly

- Exercises substantial control over a reporting company or

- Owns or controls at least 25 per cent of the company’s ownership interests.

Beneficial owners must be natural persons, meaning that trusts, corporations, or other legal entities do not qualify. However, under specific circumstances, information about an entity may be reported instead of information about an individual beneficial owner.

Substantial Control and Ownership Interest

Substantial control over a reporting company can be exercised in several ways:

- Being a senior officer (e.g., president, CFO, general counsel),

- Having authority to appoint or remove a majority of directors or certain officers

- Being an important decision-maker or

- Having any other form of substantial control.

An individual is considered an important decision-maker if they make decisions about a company’s business, finances, and structure, thus exercising substantial control over the reporting company.

Ownership interest generally refers to any arrangement that establishes ownership rights in a company, such as shares of equity, stock, voting rights, or other mechanisms.

Illustrations to understand the Beneficial owner

We will identify the beneficial owners from the examples.

Illustration 1: LLC owned and controlled by a single person

ABC company is a limited liability company (LLC) where individual A is the CEO and sole owner of the company. He is engaged in making important decisions for the company . No one else owns or controls the ownership interest in the company or exercises substantial control over the company.

Individual A is the beneficial owner of ABC LLC as :

- He owns more than 25 percent or more of the shares of ABC LLC.

- He is the CEO of the company exercising substantial control over the company.

Illustration 2: Corporation owned and controlled by a different person

ABC company is a corporation where individuals A, B and C own 50 percent,35 percent and 15 percent of the stock. Another Individual D is the CEO of the company but does not own any stock.

Individuals A,B and D are the beneficial owners of the company whereas Individual C is not the beneficial owner.

- Individual A and B is the beneficial owner of ABC company as they owns more than 25 percent or more of the shares of the company.

- Individual C is not the beneficial owner of ABC company as he owns less than 25 percent or more of the shares of the company and he is not the senior officer of the company.

- Individual D is CEO of the company. As a senior officer of the company, Individual D exercises substantial control over the company and is therefore a beneficial owner.

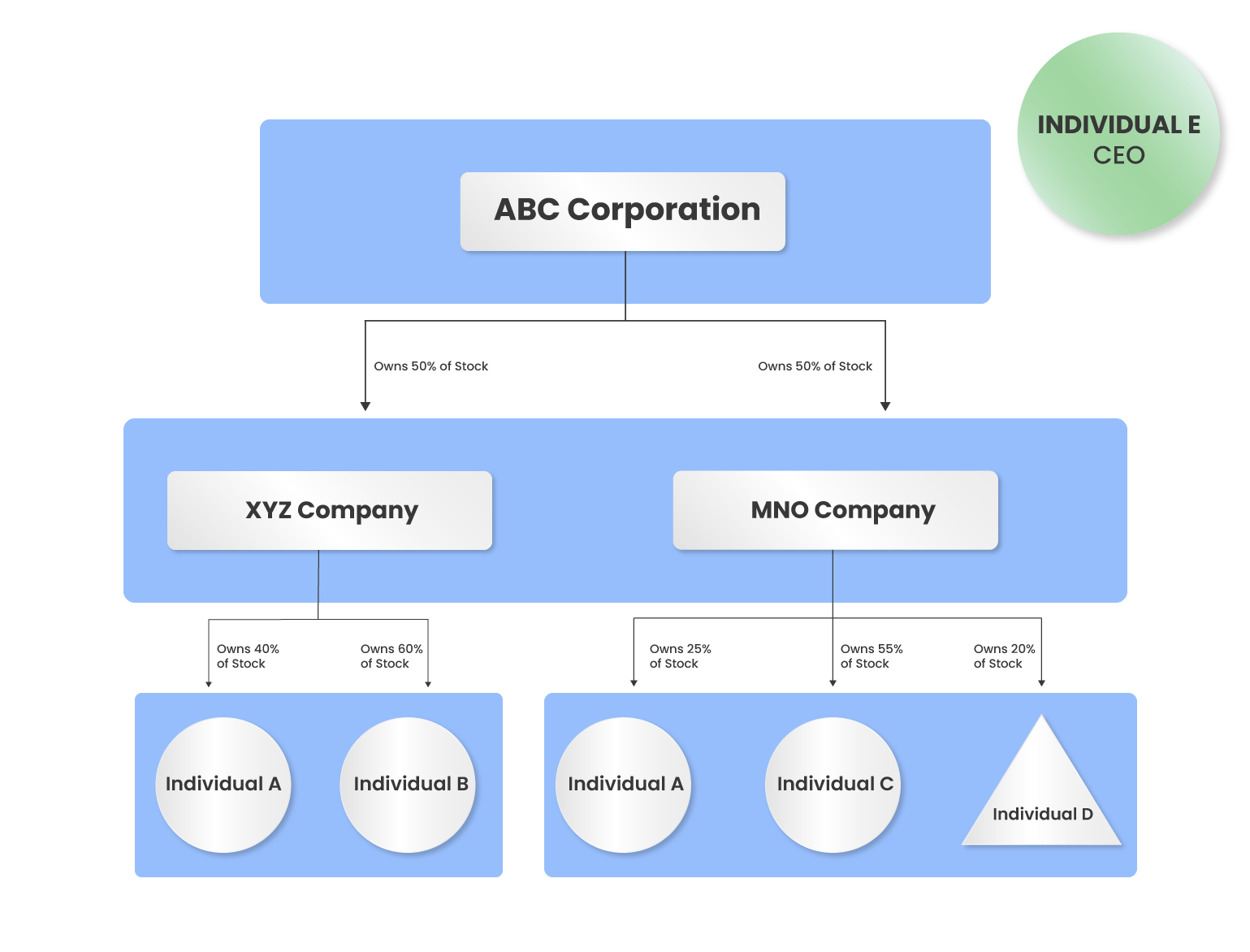

Illustration 3: Corporation owned and controlled by another company with multiple indirect owners

ABC Corporation is equally owned and controlled by XYZ company and MNO Company. XYZ company is further owned by Individual A (40% of stock) and Individual B (60% of stock) whereas MNO company is owned by by Individual A (25% of stock), Individual C (55% of stock) and Individual D (20% of stock) and Individual E is the CEO of the ABC corporation.

Individuals A,B,C and E are the beneficial owners of the company whereas Individual D is not the beneficial owner.

- Individual A,B and C are the beneficial owner of ABC company as they owns more than 25 percent or more of the shares of the company.

- Individual A owns 40% of XYZ company and 25% of MNO company hence owning 32.5% (50*0.40+50*0.25 = 32.5%) of the stock of ABC Corporation.

- Individual B owns 60% of XYZ company and hence owning 30% (50*0.60= 30%) of the stock of ABC Corporation.

- Individual C owns 55% of MNO company and hence owning 27.5% (50*0.55= 27.5%) of the stock of ABC Corporation.

- Individual E is CEO of the company. As a senior officer of the company, Individual E exercises substantial control over the company and is therefore a beneficial owner.

Exceptions to the Beneficial Owner Definition

There are five specific instances where an individual who would otherwise be a beneficial owner qualifies for an exception, and the reporting company does not have to report them as a beneficial owner.

- Minor Child

- Nominee, Intermediary, custodian or agent

- Employee

- Inheritor

- Creditor

Do the following Stakeholders qualify as a beneficial owner?

In this section, we will decide the different stakeholders closely related to the company and examine whether they are the beneficial owners or not?

Accountants and Lawyers

Accountants and lawyers are generally not considered beneficial owners unless their roles involve substantial control over the company. Those providing general services are not considered to have substantial control. However, a lawyer or accountant designated as an agent may qualify for an exception.

Reporting Ownership Through Multiple Entities

If a beneficial owner holds their ownership interests through multiple exempt entities, the names of all those exempt entities may be reported to FinCEN instead of the individual’s information, provided the interests are held exclusively through these exempt entities.

Unaffiliated Service Providers

An unaffiliated company managing a reporting company’s day-to-day operations without making decisions on important matters is not a beneficial owner. However, individuals within such a company who exercise substantial control must be reported as beneficial owners.

Board Members and Beneficial Ownership

A board member is not automatically a beneficial owner. Each director’s status must be evaluated based on whether they meet the criteria of substantial control or ownership interests.

Partnership Representatives and Tax Matters Partners

A partnership representative or tax matters partner of a reporting company is not automatically considered a beneficial owner. However, they may qualify as a beneficial owner if they exercise substantial control or own/control at least 25 percent of the company’s ownership interests.

Ownership Disputes

In cases of ownership disputes, the reporting company must report all individuals who exercise substantial control or claim ownership/control of at least 25 percent of the company’s interests. Updates must be filed if litigation results in changes to the beneficial ownership.

Corporate Entity Ownership

If a corporate entity owns or controls 25 percent or more of a reporting company’s interests. In that case, the individuals who indirectly exercise substantial control or own/control at least 25 percent through the entity must be reported.

Homeowners Associations

Homeowners associations that meet the reporting company definition and do not qualify for exemptions must report beneficial owners, which includes individuals who exercise substantial control or own/control at least 25 per cent of the ownership interests.

Trusts and Beneficial Ownership

Beneficial owners can own or control a reporting company through trusts by exercising substantial control or owning/controlling ownership interests held in a trust. The specifics depend on the trust arrangement and the roles of trustees, beneficiaries, grantors, and settlors.

Corporate Trustees

When ownership interests are held through a trust with a corporate trustee, the reporting company should determine if the corporate trustee’s individual beneficial owners indirectly own or control at least 25 per cent of the reporting company’s interests. Special rules apply if certain conditions are met.

Entities Owned by Indian Tribes

For entities owned by Indian Tribes, the nature of the entity affects whether it must report beneficial ownership information. Tribes themselves are not reported as beneficial owners, but individuals exercising substantial control or owning/controlling significant ownership interests may need to be reported, depending on the specific circumstances.

Information required for Beneficial Owners

For each beneficial owner, companies must report:

- Name

- Date of Birth

- Residential Address

- Identification Number: This number should come from an acceptable ID document such as a passport or a US driver’s license or a identification document issued by a state, local government or tribe. An image of the identification document must also be provided.

Understanding Company Applicants: Key Points for Reporting Companies

In this section, we will discuss the reporting requirements for company applicants, identify who qualifies as a company applicant, and determine whether company applicants can be excluded from the BOI report.

Reporting Requirements to report the company Applicants

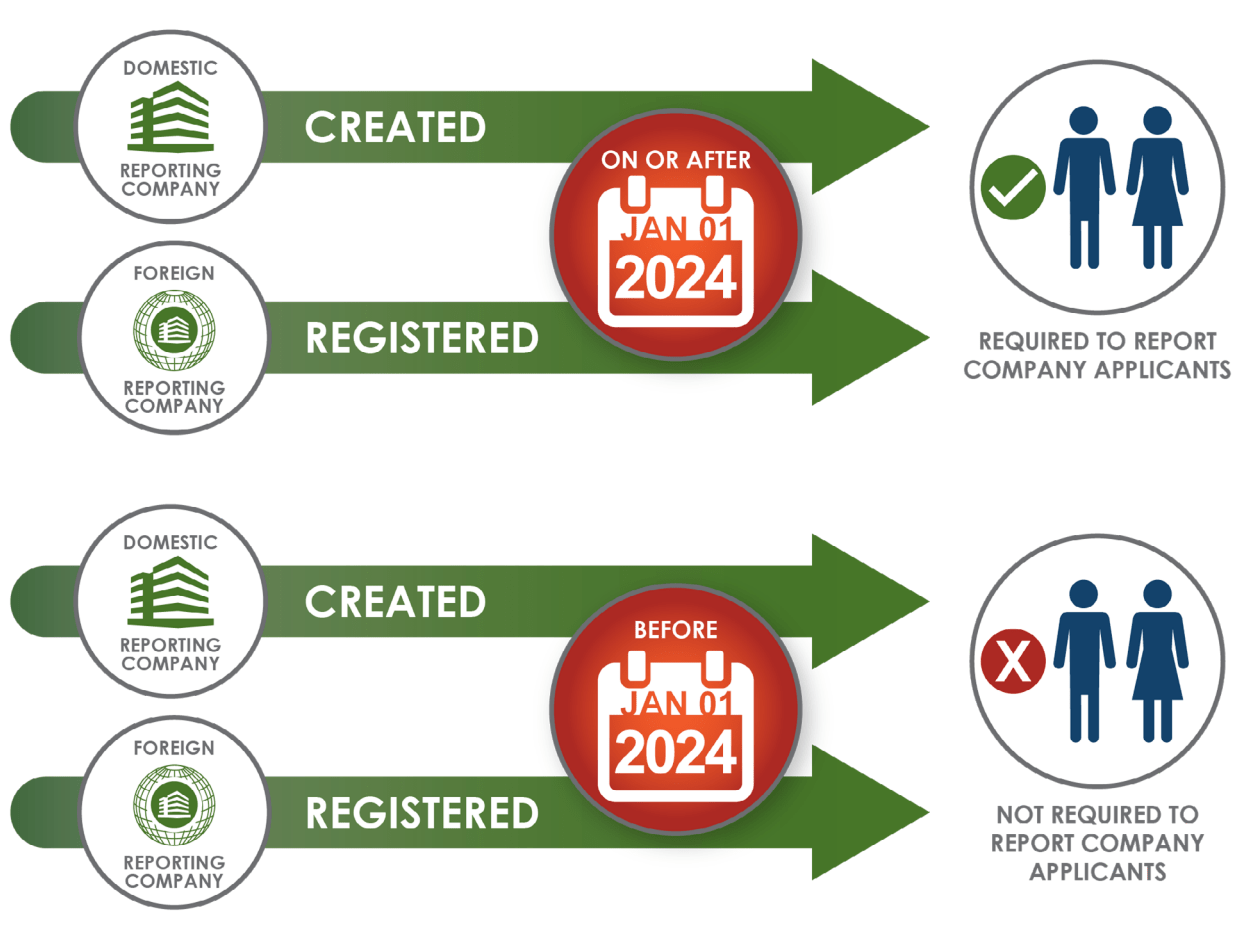

The requirement to report company applicants does not apply to all reporting companies.

Specifically, only those companies that are domestic reporting companies created in the United States on or after January 1, 2024, or foreign reporting companies first registered to do business in the United States on or after that date need to report their company applicants.

Companies established before January 1, 2024, or foreign companies first registered to do business in the US before this date are exempt from this reporting obligation.

Who is a Company Applicant?

For reporting companies established or registered on or after January 1, 2024, identifying and reporting company applicants is a crucial requirement. A company can designate at least one company applicant and at most two individuals. Only Individuals can be a company applicants whereas Companies or legal entities cannot be company applicants.

There are two categories of company applicants which are as under:

Category 1 Company Applicant : Direct Filer

The first individual is the one who directly files the document that creates a domestic reporting company or registers the foreign reporting company. This individual is the one who have actually physically or electronically filed the document with the secretary of state or similar office.

Category 2 Company Applicant : Directs or controls the filing action

If multiple people are involved in the filing process, the second individual to be reported is the one who is primarily responsible for directing or controlling the filing. This individual is a company applicant even though the individual did not actually file the document with the secretary of state or similar office.

Determining Primary Responsibility

When determining who is “primarily responsible” for directing or controlling the filing of the creation or registration document, it is important to consider who made the substantive decisions about the filing, including its management, content, and timing.

For instance, if an attorney prepares a company creation document and directs its filing, the attorney and the individual who files the document with the relevant office are both considered company applicants. This principle holds even if a paralegal or another subordinate completes the actual filing at the attorney’s direction.

Further Illustration for Company Applicant

Example 1: Individual A is creating a new company who prepares the necessary documents and files them with the relevant State or Tribal office, either in person or using a self-service online portal. No one else is involved in preparing, directing, or making the filing.

Individual A is the only company applicant because Individual A is the only person involved in the filing. State or Tribal employees who receive and process the company creation or formation documents should not be reported as company applicants

Example 2: Individual A prepares the necessary documents to create the company and directs Individual B to file the documents with the relevant State or Tribal office. Individual B then directly files the documents that create the company.

Individuals A and B are both company applicants as Individual A was primarily responsible for directing or controlling the filing whereas Individual B directly filed the documents.

Whether Accountants and Lawyers are Company Applicant?

The role of accountants and lawyers in the filing process can determine if they qualify as company applicants. If an accountant or lawyer directly files the creation or registration document for a reporting company, they may be considered a company applicant.

Additionally, if there are multiple individuals involved in the filing, the accountant or lawyer who primarily directs or controls the filing process also qualifies as a company applicant. For example, if an attorney at a law firm oversees and directs the preparation of incorporation documents, both the attorney and a paralegal who files these documents are considered company applicants.

Are third-Party Couriers considered company applicant?

Third-party couriers or delivery service employees who only deliver documents to the relevant authorities are not considered company applicants. These couriers simply facilitate the delivery of documents and do not participate in the creation or registration process beyond this role. Instead, the individual who requested the courier’s services will typically be recognized as the company applicant. However, if a courier is employed by a business formation service that is actively involved in drafting or managing the documents, the courier may be considered a company applicant due to their closer involvement in the process.

Who is the company applicant while using automated incorporation services to file the creation or registration documents for a reporting company?

If an individual uses an automated incorporation service, such as an online platform, to file the creation or registration documents for a reporting company, the individual using the service is the company applicant. Automated services that provide software or guidance but do not directly participate in filing do not have employees who qualify as company applicants. Therefore, in cases where a person self-files using such services, only that individual is reported as the company applicant.

These guidelines ensure clarity in the reporting process and help maintain accurate records for reporting companies.

How to remove company applicants from BOI Reports?

Once a company applicant is reported in the initial Beneficial Ownership Information (BOI) report, they cannot be removed even if they no longer have a relationship with the reporting company. This is because a reporting company created on or after January 1, 2024, is only required to file its initial BOI report and is not obligated to update it if there are changes regarding company applicants.

Information Required for Company Applicants

Company applicants’ details must include:

- Name

- Date of Birth

- Address

- Identification Number: From an acceptable ID document similar to those used for beneficial owners. An image of this document is also required.

If the company applicant is involved in corporate formation, such as an attorney or formation agent, their business address must be reported. Otherwise, the reporting should include their residential address.

Reporting Timeline For Initial Report

FinCEN began accepting BOI reports on January 1, 2024. Reports can only be submitted electronically through FinCEN’s secure BOI E-Filing website.

The filing process is designed to be straightforward, with the necessary form available on FinCEN’s BOI E-Filing website. Companies may choose authorised individuals such as third-party service providers to file the BOI on behalf of the company. Filers must provide basic contact information, including their name and email address or phone number.

Determining the Date of Creation or Registration

The date of creation or registration is the earlier of the following:

- The date the company receives actual notice that its creation or registration has become effective.

- The date when a public notice is provided by a secretary of state or similar office.

This process can vary depending on state practices, with some states providing automated notices and others relying on public postings.

Compliance and Enforcement: Understanding the Consequences of Non-Compliance

Reporting companies are required to report, update, and correct their beneficial ownership information as mandated. If a company fails to adhere to these obligations, FinCEN is committed to enforcing compliance through both civil and criminal penalties. While FinCEN acknowledges that this is a new requirement and offers some leniency, specifically a 90-day grace period to correct mistakes or omissions, persistent non-compliance can lead to serious consequences.

Penalties for Violating BOI Reporting Requirements

Under the Corporate Transparency Act, individuals who willfully violate BOI reporting requirements may face significant penalties:

- Civil Penalties: Up to $500 per day for each day the violation continues, with adjustments for inflation. As of the latest update, this amount is $591.

- Criminal Penalties: Up to two years of imprisonment and fines up to $10,000 for willful violations, including failure to file, submitting false information, or not correcting reported information.

These penalties underscore the importance of compliance and accurate reporting.

Liability for Violations

Both individuals and corporate entities can be held accountable for willful violations of the BOI reporting requirements:

- Corporate Entities: A company can be liable for failing to report accurate or complete information.

- Individuals: Individuals who willfully file false information, provide false information to the filer, or are senior officers at the time of non-compliance can also be held responsible.Those who file reports on behalf of a company can face the same penalties as the company and its senior officers.

- Beneficial Owners and Company Applicants: Individuals who withhold required information from the reporting company can be held liable if their actions result in the company failing to submit accurate or updated information.

It is the responsibility of the reporting company to ensure the accuracy of the information it submits to FinCEN, regardless of the source of that information. Companies must verify details provided by beneficial owners and company applicants and certify that their reports are accurate and complete at the time of filing.

If a beneficial owner or company applicant withholds necessary information, the reporting company must take proactive measures to ensure complete and accurate reporting. Companies should communicate the importance of compliance to their beneficial owners and establish mechanisms to keep information current. Beneficial owners and company applicants also need to be aware that their failure to provide required information could lead to penalties.

Updating Beneficial Ownership Information Report

In this section, we will delve into how the BOI report can be updated and explore the various scenarios in which the BOI needs to be updated.

Timeliness for Reporting Changes

If there are changes to the information previously reported in a beneficial ownership information (BOI) report, companies must file an updated report within 30 days of the change. This requirement ensures that FinCEN has the most current information about the company and its beneficial owners.

Note: Companies are not required to update the report for changes related to company applicants.

Common Triggers for Updating the Report

Several scenarios might trigger the need for an updated BOI report, including:

- Changes to Company Information: This includes updates such as a new business name or changes in the company’s registration details.

- Changes in Beneficial Ownership: This could be due to new beneficial owners joining the company or changes in ownership percentages.

- Updates to Beneficial Owners’ Details: This encompasses changes to a beneficial owner’s name, address, or identification number. For example, if a beneficial owner updates their driver’s license or other identifying documents, these changes must be reflected in the updated report, including a copy of the new document.

Reporting Changes in Ownership Interest

If the type of ownership interest held by a beneficial owner changes—such as converting preferred shares to common stock—this does not necessitate an updated BOI report. FinCEN does not require reporting the type of ownership interest, only changes to the beneficial ownership information itself.

For more information, see Chapter 6 of FinCEN’s Small Entity Compliance Guide.

Updating the Report with Partial Changes

When updating a BOI report due to a change like a new legal name, the reporting company must complete the entire report. This includes submitting all fields, not just the updated information. Companies that previously used the fillable PDF format can update their saved copy and resubmit it. If the web-based application was used, a new report must be submitted in full, either through the web-based application or by uploading the updated PDF version.

Handling Late Updated Reports

Updated BOI reports can be submitted at any time, but they must be filed within 30 days of the change. Companies should ensure timely communication with third-party service providers to meet the 30-day deadline if these providers handle report submissions.

Reporting the Loss of Exempt Status

If a reporting company that filed a “newly exempt entity” BOI report later loses its exempt status, it must file an updated BOI report reflecting the current beneficial ownership information. This ensures that FinCEN’s records are accurate and up-to-date.

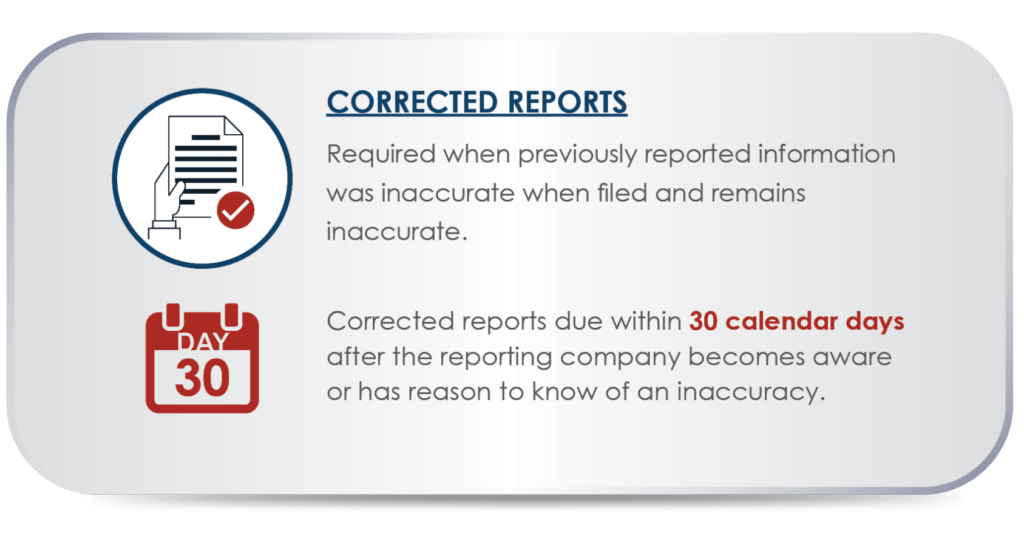

Correcting Inaccuracies in the Report

If you discover an inaccuracy in a BOI report, it must be corrected within 30 days from when the company became aware of or should have been aware of the inaccuracy. This applies to any errors in the reported information about the company, its beneficial owners, or its company applicants.

Newly Exempt Entity Report

When a reporting company that has previously filed a beneficial ownership information (BOI) report becomes exempt from further filing requirements, it must update its status with FinCEN. The company should file an updated BOI report to reflect its new exempt status.

Required Actions for Exempt Status

To properly document its exemption, the company’s updated BOI report should include the following:

- Identification of the Entity: The report must clearly identify the company that has become exempt.

- Exempt Status Declaration: The company should check a specific box or option in the report that indicates its newly acquired exempt status.

By following these steps, the company ensures that FinCEN’s records are accurate and up to date regarding its reporting obligations.

Special Considerations for Exempt Companies Losing Status

For companies created or registered before January 1, 2024, that lose their exempt status between January 1, 2024, and January 1, 2025, they must file their initial BOI report within 30 calendar days of losing their exempt status. However, they are granted the longer of the following two periods:

- The remaining time in the one-year filing period for companies existing before 2024.

- The 30-calendar-day period for companies losing exempt status.

For example, if an exempt company loses its status on February 1, 2024, it has until January 1, 2025, to file its report. If the loss of status occurs on December 15, 2024, the report is due by January 14, 2025.

Understanding the FinCEN Identifier

The FinCEN identifier is an essential tool provided by the Financial Crimes Enforcement Network (FinCEN) to streamline the reporting and identification process for individuals and companies. Let’s delve into what a FinCEN identifier is, its usage, and the process of obtaining one.

Definition of FinCEN Identifier

A FinCEN identifier is a unique identifying number issued by FinCEN to an individual or a reporting company upon request. This identifier is granted after the applicant provides specific information to FinCEN.

Each individual or reporting company is eligible to receive only one FinCEN identifier. A FinCEN identifier is not mandatory for individuals or reporting companies.

Using a FinCEN Identifier

Once obtained, a FinCEN identifier can be used by reporting companies to substitute the personal information of a beneficial owner or company applicant on a beneficial ownership information report. This identifier can replace the required personal information, simplifying the reporting process.

Additionally, a reporting company can use another entity’s FinCEN identifier and full legal name instead of providing information about its beneficial owners under three conditions:

- The other entity must have a FinCEN identifier and share it with the reporting company.

- The beneficial owners must hold interests in the reporting company through ownership interests in the other entity.

- The beneficial owners of both the reporting company and the other entity must be the same individuals.

Requesting a FinCEN Identifier

Individuals can request a FinCEN identifier starting January 1, 2024, by completing an electronic web form available at FinCEN’s website. The required information includes:

- Full legal name

- Date of birth

- Address

- Unique identifying number and issuing jurisdiction from an acceptable identification document

- An image of the identification document

Upon submission, the individual will immediately receive a unique FinCEN identifier.

Reporting companies can request a FinCEN identifier by checking a box on the beneficial ownership information report upon submission. If the request is made after the initial report, an updated beneficial ownership information report must be submitted to obtain the identifier.

Access to Beneficial Ownership Information

FinCEN’s phased approach to providing access to beneficial ownership information is designed to ensure security and efficiency. Here’s a detailed look at the timeline, eligibility, and preparations needed for authorized recipients.

Phased Access Timeline

FinCEN will gradually roll out access to beneficial ownership information through the following phases:

- Spring 2024: A pilot program for a select group of Federal agency users.

- Summer 2024: Access extended to Treasury offices and other Federal agencies engaged in law enforcement and national security activities with existing memoranda of understanding for Bank Secrecy Act information.

- Fall 2024: Access broadened to additional Federal agencies involved in law enforcement, national security, and intelligence, as well as State, local, and Tribal law enforcement partners.

- Winter 2024: Access provided to intermediary Federal agencies for foreign government requests.

- Spring 2025: Access extended to financial institutions subject to customer due diligence requirements and their supervisors.

Currently, FinCEN is not accepting requests for access to beneficial ownership information. Future guidance will be provided on how to request access.

Requesting Information as a Federal Agency

Federal agencies involved in national security, intelligence, or law enforcement, as well as Federal regulatory agencies overseeing financial institutions’ compliance with customer due diligence, can request beneficial ownership information. These agencies must first enter into a memorandum of understanding with FinCEN to ensure the protection of the information’s security and confidentiality.

Agencies should review the Beneficial Ownership Information Access and Safeguards Rule to familiarize themselves with the requirements for accessing beneficial ownership information.

State and Local Agency Requests

State, local, and Tribal law enforcement agencies can request beneficial ownership information from FinCEN if they have a court order from a competent jurisdiction authorizing the request for a criminal or civil investigation. These agencies must also meet access requirements, including entering into a memorandum of understanding with FinCEN to safeguard the information.

State regulatory agencies supervising financial institutions for compliance with customer due diligence requirements can also request beneficial ownership information under similar conditions.

Access for Foreign Governments

Foreign governments do not have direct access to FinCEN’s beneficial ownership IT system. Instead, they can request information through intermediary Federal agencies. These requests can be made under an international treaty, agreement, or convention, or by a trusted foreign country’s law enforcement, judicial, or prosecutorial authority as determined by FinCEN, with concurrence from the Secretary of State and consultation with the Attorney General.

Foreign requests for beneficial ownership information are not currently being processed.

Preparing to Receive and Use Beneficial Ownership Information

Authorized recipients need to prepare thoroughly to handle beneficial ownership information. Preparations include:

- Establishing standards and procedures to protect information security and confidentiality, and training personnel accordingly.

- Providing FinCEN with initial and annual reports on the standards and procedures for ensuring information security and confidentiality.

- Semi-annual certification by the agency head that security and confidentiality standards are implemented.

- Setting up a secure system for storing beneficial ownership information.

- Maintaining a permanent, auditable record of information requests and disclosures.

- Conducting annual internal audits to verify appropriate use of the information and cooperating with FinCEN’s annual audits.

Supervisory Expectations for Financial Institutions

Although financial institutions subject to customer due diligence requirements are not yet required to access the beneficial ownership IT system, they should be aware that access will be extended to them in spring 2025. FinCEN will provide additional guidance on specific supervisory expectations for these institutions before they receive system access.

Conclusion

The introduction of BOI reporting is a crucial step towards promoting transparency and combatting financial crimes such as money laundering and tax evasion. The requirements apply to both domestic and foreign companies registered to do business in the United States. Each reporting company must submit detailed information about the company and its beneficial owners. This guide provides an in-depth look into the various aspects of BOI, including its importance, who must report, how to report, and who has access to the information. By understanding and adhering to these requirements, companies can help protect the integrity of the financial system and comply with federal regulations designed to deter illicit activities.

Frequently Asked Questions

Reporting companies must comply with various reporting requirements depending on their creation or registration date. Companies established on or after January 1, 2024, are required to report not only information about their beneficial owners but also details about their company applicants as discussed above. This is a significant addition to the reporting requirements for companies created before this date, which only need to report information about themselves and their beneficial owners.

To meet reporting requirements, acceptable forms of identification include:

- Non-expired U.S. driver’s license

- Non-expired state or local government-issued ID

- Non-expired U.S. passport

- Non-expired passport from a foreign government (if no other acceptable IDs are available)

This information is crucial to ensure that the reported identification is valid and meets FinCEN’s standards.

Companies are not required to report beneficial ownership information annually. Instead, they must file an initial BOI report and update or correct it as necessary. FinCEN’s Small Entity Compliance Guide provides further details on when to file these reports.

Typically, a reporting company is not required to provide information about its parent or subsidiary companies. However, if a special reporting rule applies, the company may report its parent company’s name instead of the individual beneficial owners if the owners’ interests are held through the parent, and the parent company is exempt.

A reporting company must use a US Street address for its principal place of business and cannot use a PO box. If the company lacks a US principal address, it should report the location where it conducts business or, if applicable, the address of its registered agent.

Disregarded entities, which are not treated as separate entities for US tax purposes, must report a valid TIN. Depending on their structure, they can report an EIN, SSN, ITIN, or a foreign tax identification number. The specific TIN to be reported depends on the entity’s ownership and structure.

These detailed requirements are designed to ensure transparency and compliance with FinCEN regulations, providing clarity for companies in their reporting obligations.

A parent company cannot file a single BOI report on behalf of its group of companies. Each reporting company within the group must file its own BOI report, unless exempt.

To file an initial BOI report, companies must include a tax identification number (TIN), such as an Employer Identification Number (EIN), Social Security Number (SSN), or Individual Taxpayer Identification Number (ITIN). Foreign companies must provide a tax identification number from their home jurisdiction.

The IRS offers a free online application for an EIN, which is processed immediately. If needed, companies can apply for an EIN by submitting Form SS-4. For expedited processing, fax submissions typically receive an EIN in about four business days, while mail submissions can take up to five weeks. In cases where the EIN is not received by the filing deadline, companies should file their report as soon as the EIN is obtained and maintain documentation of their efforts to comply.

The initial BOI report should only include information about the beneficial owners at the time of filing. Companies must update or correct their reports if there are any changes to the beneficial ownership.

Third-party service providers assist reporting companies in submitting their beneficial ownership information (BOI) reports to the Financial Crimes Enforcement Network (FinCEN) under the Corporate Transparency Act (CTA). They can manage the submission process via FinCEN’s BOI E-Filing website or through an Application Programming Interface (API).

Starting January 1, 2024, the BOI E-Filing application will provide an acknowledgment of submission success or failure. The third-party service provider will be able to download a transcript of the BOI report. Companies should obtain this confirmation from their provider to verify successful submission.

Yes, one of the key benefits of using a third-party service provider is their ability to submit multiple BOI reports simultaneously through the API, allowing for efficient and streamlined processing of submissions.